Allegations that insurance giant Manulife benefited from the sale of illegal mortgage insurance that defrauded thousands of Canadians have led to three class action lawsuits and questions in the B.C. legislature where opposition members claim that the province should have warned consumers.

The province last year fined three companies -- including Manulife Financial Corp., the Manufacturers Life Insurance Co., and Benesure Canada Inc. -- for breaking laws that govern British Columbia's insurance industry.

While Finance Minister Mike de Jong has said that nobody was harmed by the scheme, the lawyer whose firm has filed two of the class action suits says thousands of mortgage holders were defrauded, some without their knowledge.

Tony Merchant said some consumers paid an extra $600 a year. He estimates, based on material released by Manulife, that some 170,000 Canadians may have been harmed. That adds up to tens of millions a year worth of ill-gotten sales for the companies.

The individuals who were harmed, however, are hard to find. In two weeks of trying, Merchant's firm was unable to put The Tyee in touch with a single consumer who had purchased the product and was willing to talk publicly about the experience.

"There are all sorts of people who've suffered loss, but they don't know it," said Merchant. "Consumers were manipulated into buying products, paying about $50 extra per month on top of their mortgage payments."

As Merchant describes it, the companies duped people into buying mortgage insurance that was overpriced for what it covered. "Manulife appears to have been tied up with a wrongful insurance scheme which took advantage of people in significant ways and did not give them the insurance they thought they had," he said.

Saskatchewan action

In late March, the Merchant Law Group LLP Davis + Henderson LP filed a statement of claim in the Court of the Queen's Bench for Saskatchewan against the Manufacturers Life Insurance Co., Manulife Financial Corp., Benesure Canada Inc., Davis + Henderson LP and three other parties.

The lawsuit follows similar cases filed in 2013 in British Columbia and Quebec courts, which are awaiting rulings on whether they can proceed.

None of the allegations has been tested or proven in court.

Manulife's director of media relations, Rebecca Freiburger, said in an email that she couldn't comment on the lawsuits. Nor has the company yet been required to file a statement of defence in any of the three court proceedings.

In late February, New Democratic Party justice critic Mike Farnworth asked a series of questions in the B.C. legislature about a $150,000 fine, plus $31,152 in costs, that the province's superintendent of financial institutions quietly levied in 2014 against Manulife Financial Corp., the Manufacturers Life Insurance Co. and Benesure Canada Inc.

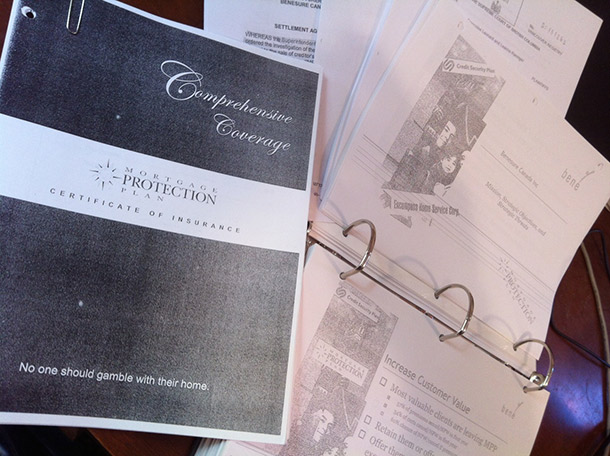

Like the lawsuits, the fine related to the Mortgage Protection Plan that the companies sold as mortgage insurance through mortgage brokers. Homebuyers sometimes purchase this kind of insurance to cover the cost of their mortgage in case death prevents them from paying.

Farnworth asked whether the government had notified people who bought mortgage insurance from the companies, the RCMP, or the insurance industry regulators in other provinces where the companies do business.

Nobody harmed: de Jong

De Jong did not immediately have answers, but a week later on March 5 he said in the legislature that the Financial Institutions Commission "found no evidence of harm to policyholders, so no press release was issued, but the consent order concluding the investigation was publicly posted on the FICOM website."

FICOM is the B.C. provincial agency that administers the laws regulating financial institutions, including insurance companies, to protect the public.

De Jong said this week that he had nothing to add to what he'd already said in the legislature.

Manulife's Freiburger said the company agrees with the B.C. regulator that there was no harm to policyholders.

The consent order included few details, but said the superintendent observed contraventions of four sections of the Financial Institutions Act, including rules that prohibit the operation of an unauthorized insurance business and the payment of commissions to unlicensed agents.

De Jong said that Financial Institutions Commission did inform other regulators in Canada, but did not contact the police since the commission had found no evidence of criminal activity.

Raises more questions: NDP

"I think the answers we got back raised more questions," Farnworth said in an interview. He asked how the investigators knew that nobody was harmed and whether they did anything to check with consumers who'd bought the insurance policy.

He questioned the decision not to notify the public.

"People should have a right to know," he said. If the information were public, then people could decide whether or not they wanted to continue to do business with companies that the regulator had found to use fraudulent practices.

Farnworth also said it should be up to the police, not the government regulator, to assess whether something criminal had taken place.

"It just strikes me things are far too cosy," Farnworth said. "The decisions from the regulator seem to be more about what's in Manulife's best interest than what's in the public's best interest."

The regulator's job is to make sure the industry is functioning the way it should be, that companies are following the law, and part of that includes being public about its findings. "From what I've seen this hasn't been particularly open or transparent."

Many were harmed: lawyer

Asked about de Jong's assertion that the companies harmed no one, Merchant said, "It's just not true. Many people were harmed and they were harmed by a sort of bait and switch that was undertaken by Benesure."

Manulife somehow became connected with Benesure and enabled the smaller company to sell insurance even though Benesure's brokers were not licensed to sell insurance, Merchant said. "Manulife facilitated Benesure doing something not permitted, we say illegal," he said, noting it was surprising that a company of Manulife's size and responsibility would be involved in such a scheme.

Companies selling life insurance have to be licensed because they are subject to rules on how they can deal with people, explained Merchant. Insurance companies have a fiduciary duty to the people they sell policies to, meaning they have to act in the best interest of the client.

Since Benesure was not licensed, its employees had no fiduciary duty, he said. "They put people into mortgage insurance that was not mortgage insurance that anyone selling life insurance would appropriately put them into."

Benesure was able to access confidential information from D+H Corp., which runs the computer system that helps mortgage brokers match customers with mortgage providers. It used the information to send "safety catch" letters that pressured people to buy their Mortgage Protection Plan (see sidebar).

Manulife benefited from the relationship with Benesure, Merchant said. "They were there in the first place because they got a whole lot of low-paid sales people."

Risk to reputation

Most people who bought the insurance likely never realized they'd been duped, said Merchant.

Nobody, including the companies and the regulators, has informed the market, he said, and nobody has volunteered to try to identify the people who were harmed. "That's what makes the minister's response so hollow."

Asked why the cases haven't had more media attention, Merchant said, "I think it's because it's too complex."

Manulife is a publicly traded company worth $40 billion. It had $54 million in revenue in 2014. Its shares are widely held, including, for example, by B.C. Justice Minister Suzanne Anton's husband, according to her 2014 financial disclosure.

The company's most recent annual report does not specifically mention the class actions related to Benesure, but does note the company is regularly involved in legal actions, both as a defendant and as a plaintiff.

"Plaintiffs in class action and other lawsuits against the company may seek very large or indeterminate amounts" and the cases may take a long time to resolve, it said. "A substantial legal liability or a significant regulatory action could have a significant adverse effect on the company's business, results of operations, financial condition and capital position and adversely affect its reputation."

Even if Manulife eventually wins, the harm to its reputation could negatively affect the company's business, "including its ability to attract new customers, retain current customers and recruit and retain employees," it said. ![]()

Read more: Rights + Justice, BC Politics, Housing

Tyee Commenting Guidelines

Comments that violate guidelines risk being deleted, and violations may result in a temporary or permanent user ban. Maintain the spirit of good conversation to stay in the discussion.

*Please note The Tyee is not a forum for spreading misinformation about COVID-19, denying its existence or minimizing its risk to public health.

Do:

Do not: