Surging oil prices were the single largest driver of early pandemic inflation raising prices on everything from gas to groceries, according to a report published last week from the Centre for Future Work.

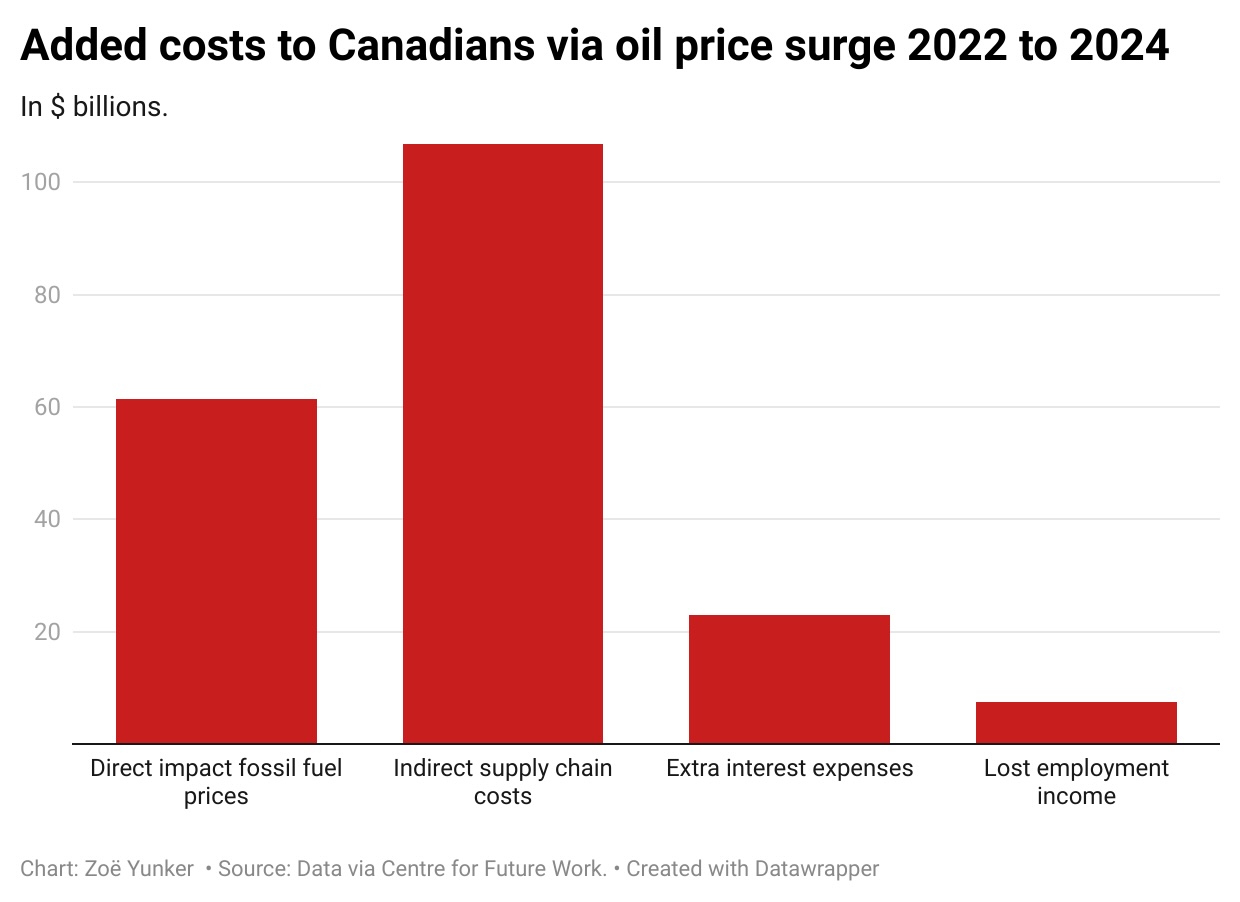

The report found that record oil company profits came at the expense of Canadians, leading to a cascade of economic shocks that cost average households $12,000 over three years.

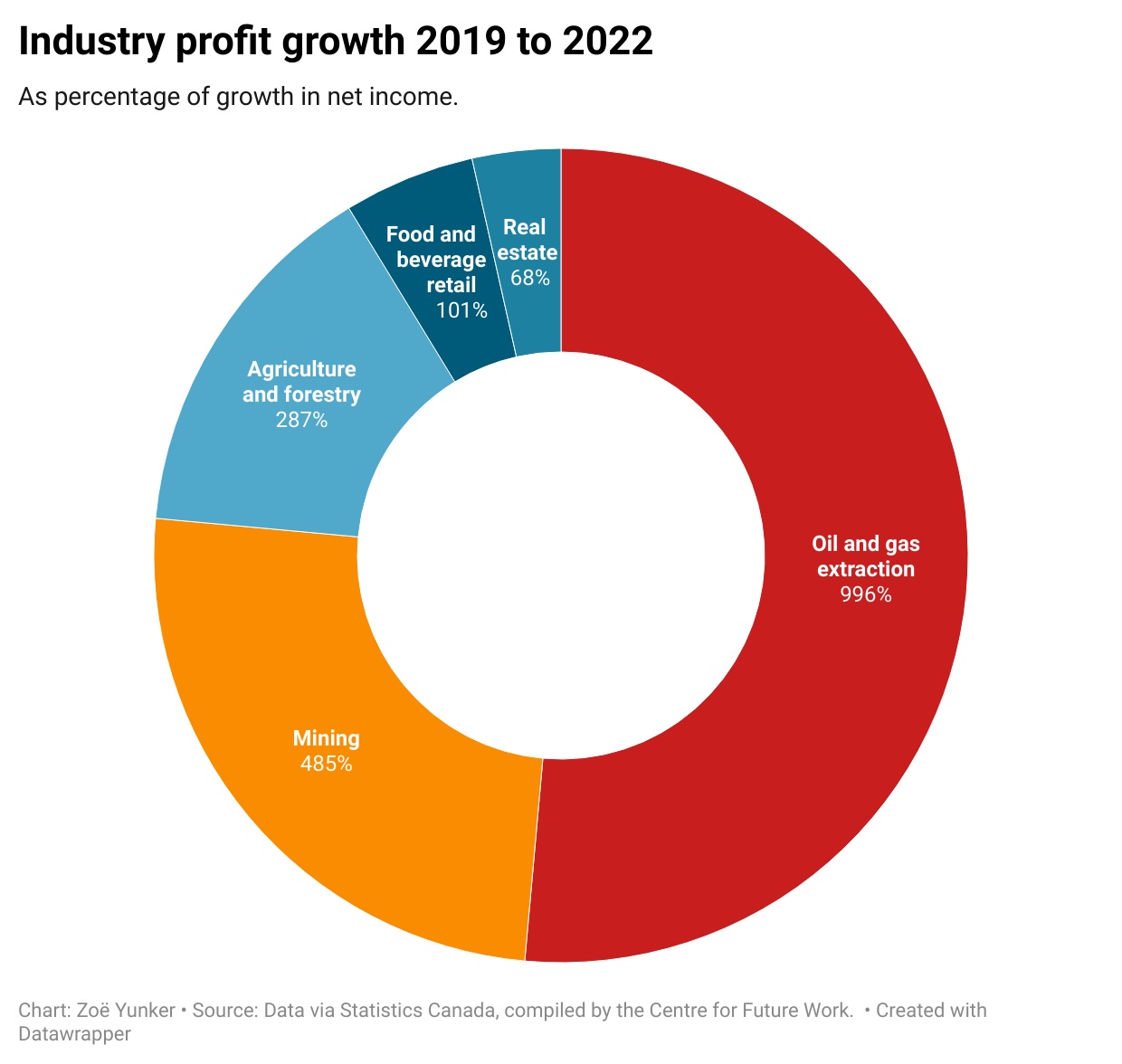

Meanwhile, industry’s profits increased almost as much as Canadians paid. All told, oil price spikes cost Canadians nearly $200 billion in three years from 2022 to the end of 2024. Over the same period, oil company profits grew by $151 billion relative to pre-pandemic levels.

“I think it’s important that we understand what happened,” economist and report co-author, Jim Stanford, told The Tyee. “Otherwise people are going to get misled into blaming other scapegoats for the problem.”

While carbon taxes became a magnet for frustration during the inflation crisis, Stanford says oil companies were actually the biggest driver of rising costs. And among the industries that profited most during Canada’s inflation surge, fossil fuel companies were in a league of their own.

The report traced the roots of the oil price spike to Russia’s invasion of Ukraine and a subsequent frenzy of speculation as traders bet on oil prices going up or down. High oil prices then filtered through Canada’s economy, triggering inflation and the Bank of Canada’s subsequent interest rate hikes. Those rates brought prices down, but at a cost, triggering job losses and higher debt payments.

With more political uncertainty on the horizon, the report warns of future price spikes ahead.

“It’s not a question of if, it’s a question of when,” said Stanford.

In the face of coming turbulence, including Trump’s tariffs on Canadian goods, provincial and federal leaders seem to be doubling down on fossil fuels. Prime Minister Mark Carney recently scrapped consumer carbon taxes and committed to accelerating new pipeline projects. Last week, Canada’s oil sector companies called on Canada to declare an “energy crisis” and scrap its cap on oil and gas emissions “to fortify Canadian independence through a stronger economy.” (Carney has since indicated he would keep the cap if elected.)

But some experts warn these moves forget the hard-won lessons of Canada’s last bout with oil price volatility. The goal, they say, should be to use less fossil fuels, not more.

Transitioning to renewable energy sources such as hydro, wind and solar “can make us less dependent on the vagaries of international markets,” said Werner Antweiler, associate professor in strategy and business economics at the University of British Columbia Sauder School of Business.

“Energy security and the energy transition go hand-in-hand.”

How did oil prices get so high, anyway?

Fossil fuel prices in Canada are tied to global markets, and they rise and fall for various reasons, including supply and demand, political instability and financial speculation.

Prices can be shaped by local influences. A recent C.D. Howe report, for example, argued Trans Mountain would reduce gasoline prices for B.C. residents. But the recent oil price spike was a global phenomenon, blowing any relative cost benefits of pipeline infrastructure out of the water.

When Russia invaded Ukraine in spring 2022, demand spiked as countries scrambled to make up for the sudden energy shortfall resulting from sanctions on Russian fossil fuels.

That short-term spike in demand was amplified by oil traders who bet on the chances of prices going up or down in the oil futures market. Although the relative impact of speculative activity remains unclear, research indicates it played a substantial role in driving up the 2022 oil price peak, which hit $130 per barrel in March 2022 — its highest price since the 2008 financial crisis.

While the spike was short-lived, receding three months later, the centre’s report found that it was enough to ripple through Canada’s economy, costing Canadians billions of dollars through the inflation that followed.

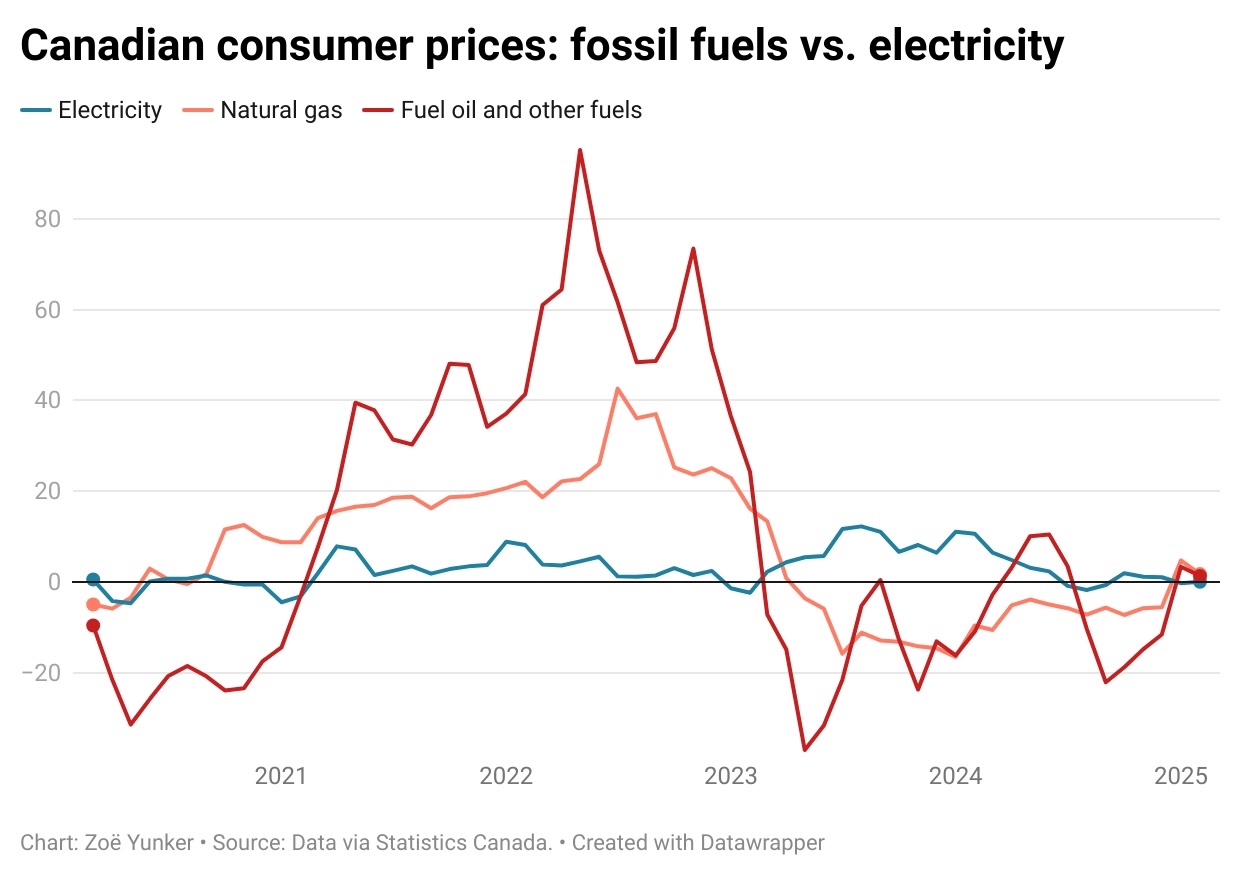

Spiking fossil fuel prices were most obvious at the gas pump, where they rose 81 per cent between January 2021 and June 2022. But that was just the tip of the iceberg, according to the centre’s report: three-quarters of the oil consumed in Canada is purchased by businesses and used to make, sell and transport their products.

Across Canada’s economy, businesses’ fossil fuel costs jumped from $6 billion in 2021 to $53 billion in 2022, and most of those costs were passed on to consumers.

According to Stanford’s analysis for The Tyee, one-sixth of the rise in grocery prices that occurred in 2022 was due to the direct impacts of more expensive fossil fuels. The increase in grocery prices has been steep. Consumers comparing individual goods have found, for example, prices double or near-double on items like cream cheese, pop and smoked ham between 2019 and 2024.

Many other items also got more expensive. To fight inflation, the Bank of Canada raised interest rates 10 times between March 2022 and July 2023. That had spill-on effects. Jobs were cut and people faced higher mortgage rates and credit card bills.

Oil companies’ profit growth was "effectively a windfall on the level of production that was already underway," said Erin Weir, an economist and co-author of the centre’s report, during a presentation.

Canada has a system to collect rents on oil and gas activity through fees called royalties. In theory, the more money companies make, the more they pay provincial and territorial governments. But provinces’ regulatory systems are full of loopholes. B.C. made almost no royalties during the windfall of 2021-22, according to the report, because the deductions it provided companies nearly matched the money it stood to gain.

And instead of investing their profits back in their businesses, the centre’s report found they went to shareholders dividends, which jumped from $8 billion to $19 billion between 2021 and 2022.

Kent Fellows, a fellow-in-residence at the C.D. Howe Institute, said there is no inherent problem with companies making more profits.

“They're a market signal of where the market wants more supply,” he said, adding that allowing companies to act freely means investors will spend their money “in ways that are going to be most effective and most profitable.” Kent, who is also an assistant professor in the School of Public Policy at the University of Calgary, noted some of those profits will be spent in Canada’s economy.

But spiking oil company profits far outpaced job outcomes. Job numbers across the oil and gas sector remained mostly static throughout the post-COVID period. At the end of 2023, the most recent data available from Statistics Canada, the sector still employed 700 people less than it did before the pandemic.

Jobs in oil and gas extraction, a subset of the sector, grew by 300 between 2019 and 2023, but wages dropped by six per cent.

“Canadian policymakers can no longer rely on the oil and gas industry to translate higher prices into more investment and more jobs,” said Weir, in his presentation.

Along with curbing royalty loopholes, Stanford and Weir’s report calls on governments to consider implementing price controls to ward against future shocks.

UBC’s Antweiler worries about the knock-on effects of manipulating prices. “We don't want to distort markets,” he said.

But Antweiler agrees with policies aimed at curbing oil profits, adding that EU countries took this approach by implementing windfall taxes during the oil price spike.

And Antweiler also concurs with the report’s final recommendation: that the most effective, long-term solution to oil price instability is ditching fossil fuels.

Switching to renewables

While oil prices surged across most of the country, electricity prices remained steady, particularly in places that rely on renewable energy sources to power their grid. And the cost of renewable energy technologies like solar and wind continues to fall.

Climate action and affordability go together, said Jessica Kelly, a senior policy advisor for the International Institute for Sustainable Development, who wrote a different report on the impacts of oil prices on inflation for the institute last year.

But that doesn’t mean energy transition will happen on its own.

Kelly wants to see more investment in technologies to make energy transition possible. That includes electric heat pumps, which can save customers money in the long term but require upfront investment. Better transit systems and electricity infrastructure to transport power through and across provinces is also required, said Kelly, but they’ll also take lots of money to build.

Meanwhile, Canada provided at least $19 billion in subsidies to fossil fuel and petrochemical companies in 2023 following the sector’s period of windfall profits.

“Even diverting a fraction of those subsidies towards energy transition solutions for households would have a significant effect on affordability,” said Kelly.

Canada did increase its funding for renewable energy technologies from $896 million to $3.3 billion between 2020 and 2023, but those totals still lagged in comparison to the full suite of financial support it provides to the fossil fuel sector.

As more political instability and climate disasters loom, Kelly wants to see the climate impacts of fossil fuels and their price volatility put onto the ledger.

“I think it’s important to weigh the costs and benefits of having this industry continue to run.” ![]()

Read more: Election 2025

Tyee Commenting Guidelines

Comments that violate guidelines risk being deleted, and violations may result in a temporary or permanent user ban. Maintain the spirit of good conversation to stay in the discussion and be patient with moderators. Comments are reviewed regularly but not in real time.

Do:

Do not: