Jason Kenney, leader of Alberta’s United Conservative Party, has vowed to dramatically cut his province’s corporate-income tax rates should he win election as premier later this spring.

Alberta’s business tax rate stands at 12 per cent of corporate income. Kenney would slash it by a third, to just eight per cent, over a four-year period.

The revenues lost soon would be made up, the UCP leader declared, through increased economic activity. In effect, Kenney’s corporate tax cuts would ‘pay for themselves.’

That optimistic messaging echoes the failed fiscal policies introduced by former British Columbia premier Gordon Campbell and his BC Liberal government at the beginning of the new millennium.

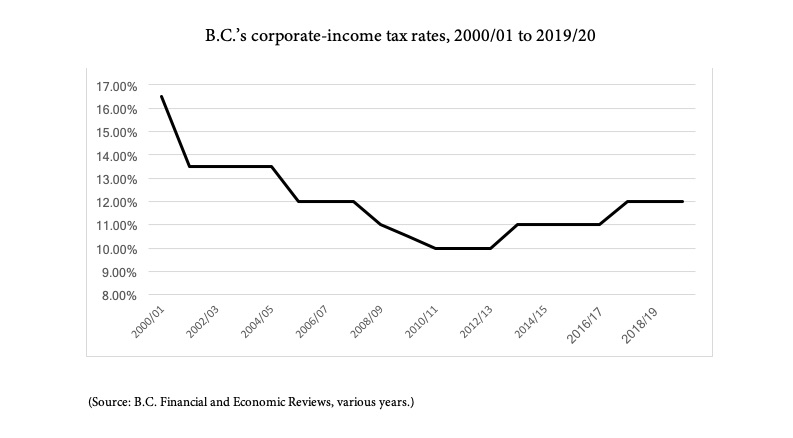

From a rate of 16.5 per cent in 2001, the Campbell Liberals quickly cut B.C.’s corporate-income tax rate to 13.5 per cent in 2002, and eventually to 10 per cent in 2011.

Campbell’s business tax cuts, however, never did pay for themselves, and instead left his province short billions of dollars of revenues. How many billions? Between $7.9 and $10.1 billion, according to calculations shared later in this piece.

Alberta’s Kenney now seems determined to lead his province down the same failed fiscal path. The journey seems likely to end with B.C.’s result: the loss of provincial revenues, and at least a partial, upward reversal in corporate-income tax rates in the not-too-distant future.

Kenney has confessed his policy — reducing Alberta’s corporate-income tax rate to the lowest in Canada — will result in a one-year loss to the provincial treasury of $348 million. Then, he claims, the tax cuts will generate over $1 billion by 2023 by stimulating new investment and jobs which in turn should produce more government revenues.

If to some Albertans that sounds too good to be true, a trip down memory lane in B.C. will offer no comfort.

BC’s teachable moment

In May 2001, Alberta’s neighbour elected a new BC Liberal government. By the summer, it had announced a flurry of tax cuts, including seven different ones for provincial businesses. Among them: slicing the corporate tax rate by one-fifth.

After the Campbell Liberals won re-election in May 2005, they further cut corporate-income tax to an even 12 per cent.

“That is four and a half points lower than when we formed government in 2001,” exclaimed finance minister Carole Taylor, who proudly reminded this kept “B.C.’s rate among the lowest in the country.”

Her government wasn’t done.

Over the course of a decade, from 2001 to 2011, Gordon Campbell and the BC Liberals pared more than a third off B.C.’s corporate-income tax rate, bottoming out at 10 per cent.

As well, the BC Liberals had taken an axe to personal income tax rates, announcing on their second day in office a 25 per cent reduction. They admitted this cut alone would deprive B.C. of $1.5 billion in revenues over a full fiscal year.

But the payoff would come, assured Christy Clark, then the minister of education and deputy premier, later to become premier. “In every jurisdiction where personal income tax cuts have been tried, they’ve worked. It’s meant more revenue to government from personal income taxes. That’s what we are going to create in British Columbia.”

Most of Campbell’s tax cuts, however, were geared toward the business sector.

Among the major — and most-costly — decreases were the elimination of the corporation capital tax for non-financial institutions, and a 50 per cent reduction in the corporation capital tax rate applied to banks and other financial-services companies.

Business purchases of equipment and machinery also were exempted from the provincial-sales tax, along with a number of other measures.

In all, the yearly cost of Campbell’s sweeping personal and corporate tax cuts was pegged at almost $1.4 billion in 2001/02, and then more than $2.1 billion in 2002/03.

And so confident were the BC Liberals that the tax reductions would “pay for themselves” that they simultaneously brought in a “balanced budget law” — in effect, outlawing fiscal deficits.

The question then, is: did Gordon Campbell’s corporate-income tax cuts work? Did the BC Liberals’ dramatic tax reductions for businesses “pay for themselves” by eventually creating more revenue for government?

Sadly, no and no.

In fact, B.C.’s corporate-income tax cuts achieved little other than to cost the provincial treasury somewhere between $8 and $10 billion.

It’s worth noting that in 2013 the BC Liberals nudged the corporate tax rate up a point to 11 per cent, where it stayed until 2017 when the NDP won B.C.’s government. The excuse given was that balancing the budget was not only a lofty goal, but required by law (see sidebar).

The truth is that from 2001/02 to 2016/17, successive BC Liberal governments racked up nine surplus budgets (five for Campbell and four for Clark) and seven deficits (five for Campbell, two for Clark). No one went to jail for breaking the law.

Another truth is that over the period that the BC Liberals governed B.C., the province’s total debt nearly doubled from $33.8 billion to $65.8 billion.

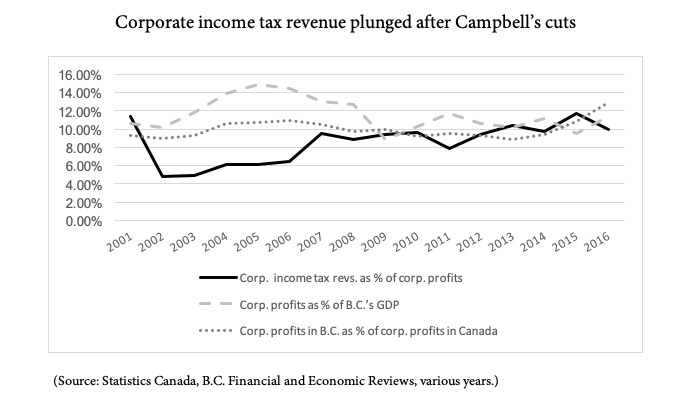

Corporate profits soared, tax revenues slumped

So ends today’s history lesson in B.C. tax politics. Let’s turn to math in order to calculate how many dollars B.C. citizens forfeited thanks to the BC Liberals’ corporate tax slashing.

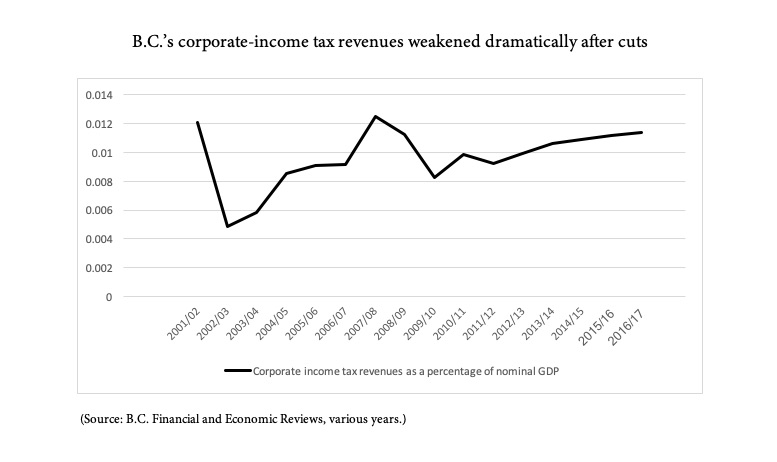

When Campbell’s BC Liberal government officially took office on June 5, 2001, corporate tax revenues were on a record pace for the province. In fact, notwithstanding Campbell’s late-fiscal year rate cut, B.C.’s corporate-income tax receipts in fiscal 2001/02 totalled nearly $1.7 billion.

That was the highest total in provincial history, mostly because corporate profits had climbed in calendar 2000 to a record $16.2 billion, and were followed in 2001 by a second-highest level, $14.5 billion.

It was somewhat ironic. Just as B.C.’s New Democratic Party — which had formed government from late 1991 through to early 2001 — was preparing to leave office, the province’s corporate profits and taxes were soaring ever higher.

Corporate profitability continued each year through nearly all of the first decade of the 21st century, hitting $14.5 billion again in 2002, and then rising steadily to $17.6 billion (in 2003), $22.5 billion (2004) and nearly $26.0 billion when B.C. voters again went to the polls in 2005.

B.C.’s economy also continued on its upward trajectory.

Nominal gross domestic product (GDP) increased steadily over the early part of the new decade, rising from $136.8 billion in 2001, to $141.9 billion (in 2002), $149.8 billion (2003), $162.3 billion (2004) and $174.9 billion (2005).

But Gordon Campbell’s drastic cuts brought an abrupt end to the province’s rising corporate tax receipts. After climbing within sight of $1.7 billion in 2001/02 — the year that marked the transition from a NDP government to a BC Liberal administration — corporate-income tax revenues fell off a cliff.

In fiscal 2002/03, corporate-income receipts plunged to just $691 million — only 42 per cent of their value in the prior year. In 2003/04, the total was an anemic $874 million, then in 2004/05, the new number was close to $1.4 billion, and in 2005/06, just under $1.6 million.

To summarize, between calendar-years 2001 and 2005 — and from fiscal-years 2001/02 to 2005/06 — B.C.’s economy grew by 27.8 per cent to $174.9 billion.

Corporate profits soared even higher, rising by 78.5 per cent to nearly $26.0 billion.

But the province’s corporate-income tax revenues slumped in the other direction, dropping by 4.1 per cent to just less than $1.6 billion.

It is painfully evident that the Campbell Liberals’ corporate-income tax cut failed to “pay for itself.”

How to determine the total cost of — that is, the total revenues lost because of — the BC Liberals’ drastically reduced tax rates on corporate incomes?

Campbell’s initial round of cuts stayed in effect, of course, from fiscal 2001/02 through to the end of 2012/13 when they dropped from 16.5 to 10 per cent.

Campbell left office in March 2011, and the government of his successor, Christy Clark, reversed course and lifted the rate to 11 per cent at the beginning of fiscal 2013/14.

The BC Liberals remained in government until mid-2017 when Clark’s administration was defeated in the Legislative Assembly.

From beginning to end, the BC Liberal Party held power in British Columbia for just over 16 years.

The task of calculating the revenues lost due to Campbell’s business-income tax reductions is somewhat challenging, because the BC Liberals in 2001 changed the province’s fiscal presentation and adopted GAAP — generally accepted accounting principles — as established by the Public Sector Accounting Board of the Canadian Institute of Chartered Accountants.

The biggest change was that B.C.’s fiscal system, which historically had focused primarily on the Consolidated Revenue Fund (CRF), was broadened to include the yearly financial results from the CRF, plus the SUCH sector — schools, universities, colleges and hospitals — as well as the net income of Crown corporations, and then combined them into a single account.

The GAAP rules came into effect in fiscal 2004/05. The Ministry of Finance later re-calculated the annual results for the fiscal years from 1998/99 to 2003/04, but subsequent accounting changes — although relatively minor — have made difficult consistent comparisons over time.

However, it is possible through the following two methods to make an approximation of the extent of B.C.’s revenue losses from Campbell’s corporate-income tax cuts.

Calculation method one: BC lost $10.1 billion

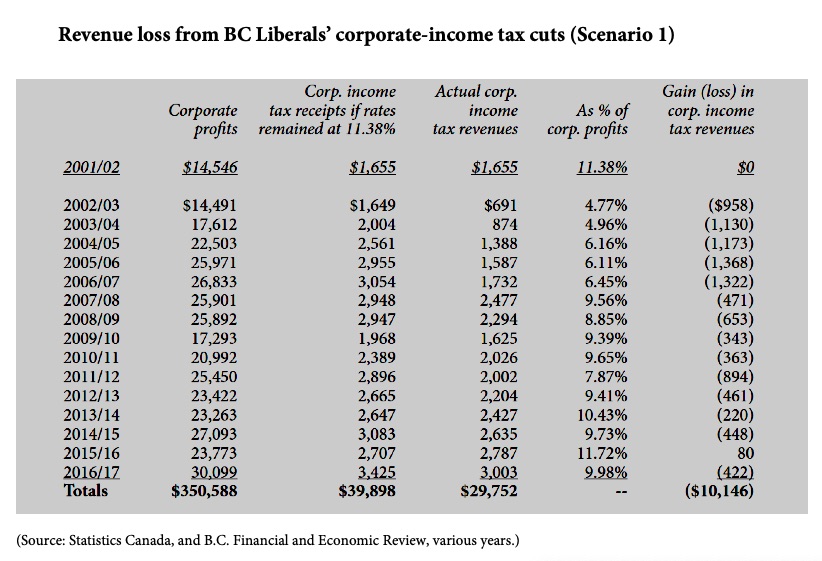

First, as mentioned previously, fiscal 2001/02 marked both the beginning of the BC Liberals’ rise to power — they were sworn into office on June 5, 2001 — and the effective date of the first reduction in the corporate tax rate: Jan. 1, 2002.

In calendar 2001, “corporation profits” — later reclassified by Statistics Canada as “net operating surplus: corporations” — in B.C. added up to $14.5 billion.

In the comparable fiscal year, 2001/02, the province’s corporate-income tax revenues totalled slightly less than $1.7 billion. That represented 11.38 per cent of the year’s corporate profits.

What if the Campbell Liberals had not slashed corporate income taxes in 2001/02, and an average rate of 11.38 per cent rate was applied to corporate profits over the remaining years in their mandate?

The answer is in the table above, which shows that B.C.’s provincial treasury, instead of taking in a 16-year total of nearly $29.8 billion, might have received a total of almost $40.0 billion.

The difference between those two numbers — more than $10.1 billion — is one measure of the monies lost through the BC Liberals’ corporate-income tax cuts.

Calculation method two: BC lost $7.9 billion

A second calculation may be performed with the assumption that B.C. did not have a change in government in 2001, or at least did not change corporate-income tax rates.

Put another way, let us suppose that the New Democratic Party had remained in office through the beginning of the new millennium, and maintained the same corporate-income tax rates as were in effect through most of the 1990s.

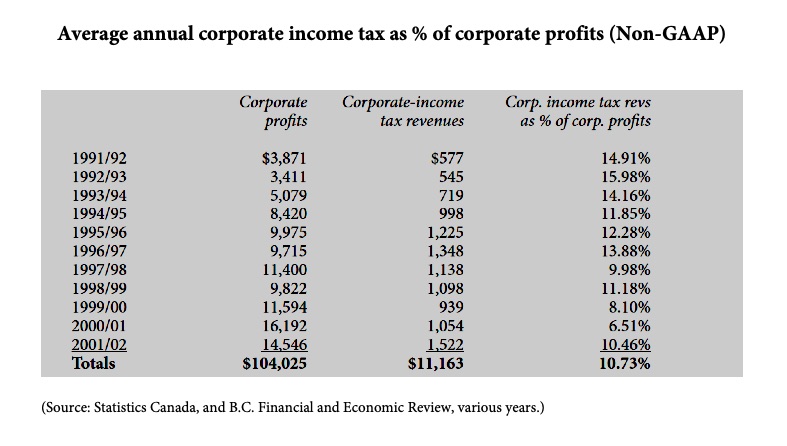

As is evident from the table above, corporation profits in B.C. through successive NDP administrations rose spectacularly from $3.9 billion in 1991/92 — the New Democrats were sworn into office on Nov. 5, 1991 — to more than $14.6 billion in 2001/02 as the BC Liberals took office on June 5, 2001.

B.C.’s corporate-income tax rate was raised by one percentage point to 16 per cent effective Jan. 1, 1992, by the New Democratic Party government, and subsequently lifted to 16.5 per cent on July 1, 1993, where it remained through to Jan. 1, 2002.

From 1991 through to the end of 2001, corporate profits earned by B.C. businesses added up to $104.0 billion. Corporate income taxes from 1991/92 until 2001/02 generated nearly $11.2 billion for the provincial treasury, an amount which represented 10.73 per cent of corporate profits.

Total business profits when the BC Liberals were in government from 2001 through to the end of 2016 added up to $350.6 billion. If the monies generated by corporate-income taxes had been equal to the 10.73 per cent of corporation profits as in the 1990s, the revenues would have been $37.6 billion.

They were not, of course, and instead came in at only $29.8 billion, a loss of almost $7.9 billion.

These two methods of calculation illustrate that Gordon Campbell’s cuts to B.C.’s corporate-income tax rates likely cost the provincial treasury something in the range of $7.9 billion to $10.1 billion over a 16-year period.

There likely are other measurements that may be made, but no method could prove that the BC Liberals’ business-tax cuts ended up “paying for themselves.”

Instead, the Campbell Liberals actually imposed a significant revenue loss on all British Columbians, denying or reducing for residents valued services such as health care, education, public safety, environmental protection, and much more. The lowest estimate of $7.9 billion forfeited revenues, for example, would have more than paid for the annual child care subsidies introduced by the current NDP government.

Plus, recall that despite passing a “balanced-budget law” in 2001, the BC Liberals over a 16-year period racked up seven deficits and just nine surpluses. And the province’s total debt, of course, nearly doubled from $33.8 billion to $65.8 billion.

It is possible that Jason Kenney has a different strategy than that used by Gordon Campbell to implement dramatic cuts to corporate-income tax rates. And perhaps Alberta’s fiscal results after Kenney’s tax-slashing will be drastically different from those experienced by British Columbia in the period 2001 to 2017.

But it seems unlikely, and so Albertans ought to prepare themselves for a string of sizeable losses in corporate-income tax revenues, a reduction in valued-public services, a string of fiscal deficits, and an ever-rising provincial debt. ![]()

Tyee Commenting Guidelines

Comments that violate guidelines risk being deleted, and violations may result in a temporary or permanent user ban. Maintain the spirit of good conversation to stay in the discussion.

*Please note The Tyee is not a forum for spreading misinformation about COVID-19, denying its existence or minimizing its risk to public health.

Do:

Do not: